Chargeback vs Refund: What's the Real Difference and When Should You Use Each?

I’ve spent years analyzing payment disputes, and the most common mistake I see, on both the consumer and merchant side, is confusing a chargeback with a refund. They sound similar. They both result in money going back to the buyer. But how they work, who controls them, and what they cost are completely different. Getting this wrong can cost merchants thousands of dollars in unnecessary fees and can leave consumers stuck in a 90-day dispute process when a two-minute phone call would have fixed everything.

Let me break this down clearly so you know exactly which path to take, and when.

What Is a Refund?

A refund is a voluntary transaction reversal initiated by the merchant. When you return an item, report a problem with an order, or qualify under a seller’s cancellation policy, the merchant sends your money back through their payment processor. It’s a direct, merchant-controlled process.

What is refunded in this scenario is straightforward: the original transaction amount, sometimes minus restocking fees or return shipping, depending on the seller’s policy. Refunds typically take 3 to 10 business days to appear, and they carry no financial penalty for the merchant beyond losing the sale.

Refunds are the preferred path for dispute resolution because they keep the relationship between buyer and seller intact and cost everyone less time and money.

What Is a Chargeback?

A chargeback is a forced payment reversal initiated by the cardholder through their bank or card network, not the merchant. When you file a chargeback, you’re essentially asking your bank to take the money back from the merchant on your behalf.

Chargebacks exist for legitimate reasons: unauthorized transactions (fraud), items never received, or products significantly not as described. But the process is adversarial by design. The merchant is notified, given a window to dispute the claim, and if they lose, they don’t just lose the sale. They pay a chargeback fee, typically between $20 and $100 per dispute, and they absorb the full transaction loss.

Chargebacks and refunds both return money to consumers, but chargebacks trigger a formal bank investigation process that can take 30 to 120 days to resolve.

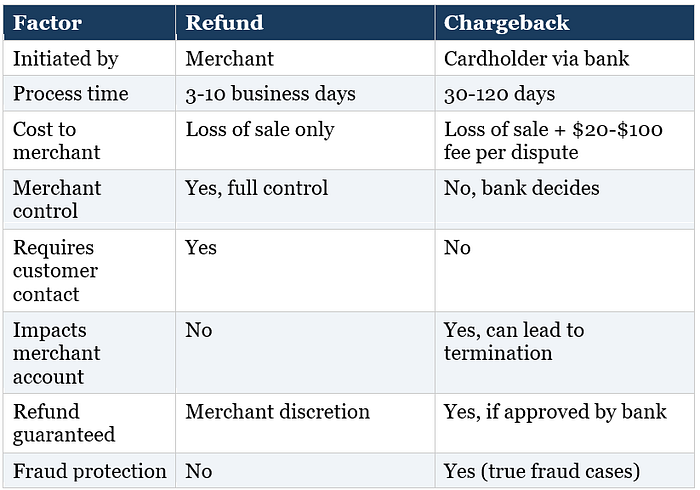

Chargeback vs Refund: Side-by-Side Comparison

Here is a structured comparison of the key differences between the two:

The Real Cost Merchants Don’t Talk About

Most merchants understand they lose the sale when a chargeback is filed. What many don’t realize is the compounding cost. According to Visa and Mastercard dispute guidelines, merchants who exceed a chargeback-to-transaction ratio of 1% enter monitoring programs. These programs impose additional monthly fines, ranging from $50 to $10,000 per month, and can ultimately result in the merchant’s account being terminated by their payment processor.

A 2024 LexisNexis report (Forrester Consulting survey) shows that for every $1 lost to fraud, merchants actually lose $3.00 once operational costs, fees, and lost merchandise are factored in. That’s not just a payment issue. It’s a business viability issue for high-volume sellers.

For consumers, filing unnecessary chargebacks (also known as friendly fraud) can result in the merchant blocking your account and, in some cases, your card issuer flagging your account for abuse. It’s not a risk-free option just because the bank is handling it.

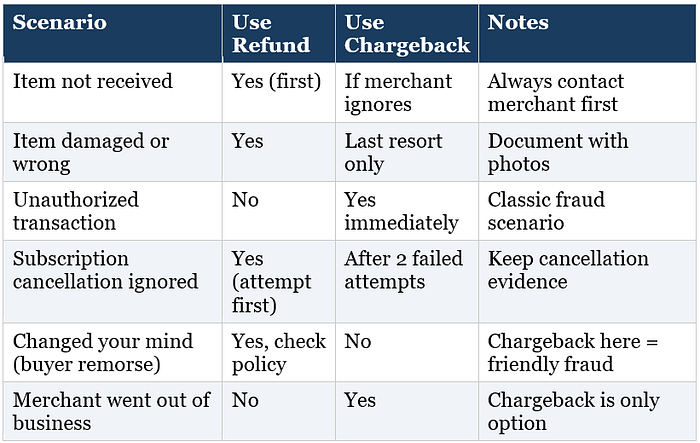

When Should You File a Chargeback vs Request a Refund?

This is the question that actually matters. The answer depends entirely on your situation:

The Return Item Chargeback: A Special Case

One scenario that trips up a lot of people is the return item chargeback. This happens when a customer returns an item and then, believing the refund is taking too long or has been denied, also files a chargeback with their bank.

This is a double-dip situation that creates a nightmare for merchants: they’ve received the returned goods and issued a refund, but now also have an open chargeback dispute. It’s technically possible for the bank to force a second refund if the merchant can’t prove the original refund was processed.

If you’ve already returned an item, wait for the refund timeline specified by the merchant (usually 5 to 10 business days) before escalating. Filing a chargeback while a refund is already in progress is likely to complicate and delay your resolution rather than speed it up.

What the Data Says About Dispute Resolution

Transaction disputes represent a major operational challenge for payment processors, often involving billions in global volume annually; streamlined automated refunds can reduce escalations when properly implemented.

Gartner’s 2023 Market Guide for Online Fraud Detection highlights rising fraud complexities, while industry reports like Chargebacks911’s 2023 Chargeback Field Report note friendly fraud as a major driver of disputes — often estimated at 70% or more of chargebacks by sources like Mastercard. This drives eCommerce investments in dispute tools. (Source)

The pattern is consistent: direct refund resolution is faster, cheaper, and better for all parties when the merchant is responsive and the dispute is legitimate.

My Practical Recommendation

If you’re a consumer: always attempt a direct refund first. Contact the seller, document everything (screenshots, emails, photos), and give them a reasonable timeframe to respond. Only escalate to a chargeback if the merchant is unresponsive, denies a clearly valid claim, or the transaction is genuinely fraudulent.

If you’re a merchant: make your refund process so smooth and clear that customers never feel the need to escalate. A well-documented, fast refund costs you only the sale. A chargeback can cost you the sale, a fee, and eventually your payment processing account.

Related Reading on BeastInsights

If you’re building a payment operations strategy, you should also explore payment fraud prevention strategies and how they integrate with your broader dispute management workflow.

For businesses dealing with subscription billing, our guide on subscription chargeback management covers the specific escalation triggers and prevention tactics for recurring payment models.

Understanding chargebacks also intersects directly with your eCommerce returns policy optimization — a clearer policy reduces buyer confusion and preempts most disputes before they escalate.